Latviešu

Latviešu По-русски

По-русски In English

In English

The battle for forests has resulted in an indefinite hiatus in transactions, with significant implications for the agricultural and forestry sectors. According to the latest "Rural Property Market Index" by "Latio," both agricultural land and forest land, which is the source of timber for the country’s primary export commodity, are facing a remarkable decline in market activity as compared to the start of the year. This slowdown is attributed to high interest rates, making it challenging for farmers to secure bank financing for land purchases. Consequently, there is a noticeable reduction in the demand for rural land. Another contributing factor to the shift in demand is the previous sale of the most valuable and fertile agricultural land plots in recent years. As a result, these sought-after plots will not be seeking for new owners that soon. This trend further impacts the dynamics of the rural land market. Simultaneously, events unfolding in Europe have cast a shadow over the forest properties segment, leading to a decrease in demand for timber produced in Latvia. At the beginning of the year, the average price for forest property stood at 4,292 EUR per ha. However, the latest data indicates a significant drop to 3,306 EUR per ha. Notably, the total number of transactions in this sector has declined by 31% compared to the third quarter of the previous year. These shifts underscore the complex interplay of factors influencing the dynamics of both agricultural and forest land markets.

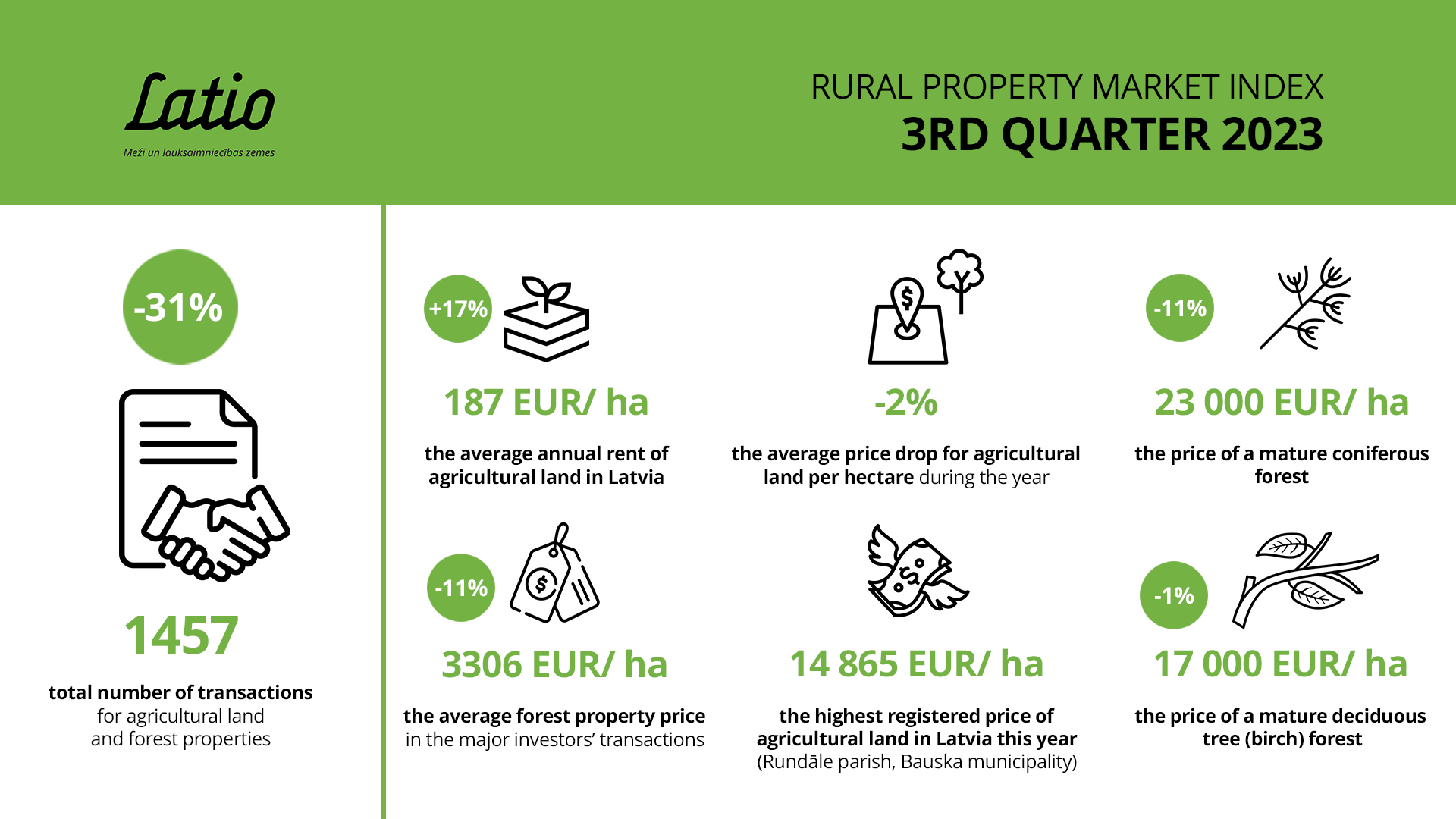

The latest data of the "Rural Property Market Index"* for the 3rd quarter of this year:

• 1457 - total number of transactions for agricultural land and forest properties (- 31% compared to the same period last year)

Agricultural land:

• 187 EUR/ ha – the average annual rent of agricultural land in Latvia (+17%)

• 14,865 EUR/ ha – the highest registered price of agricultural land this year (transaction in August - Rundāle Civil Parish, Bauska Region)

• -2% - the average price drop for agricultural land per hectare during the year (Q3 2023 against Q3 2022)

Forest properties:

• 23,000 EUR/ ha - the price of a mature coniferous forest (-11% compared to the 3rd quarter of last year)

• 17,000 EUR/ha – the price of a mature deciduous tree (birch) forest (-1%)

• 3306 EUR/ ha – the average forest property price in the major investors’ transactions (-11%)

Upon analyzing transactions involving high-quality agricultural lands measuring 3 hectares, it was determined that the average price per hectare did not undergo significant change throughout the year. There was a 2% decrease, from 3,986 EUR/ha in the third quarter of last year to 3,888 EUR/ha in the third quarter of this year. Presently, the average rent for agricultural land in Latvia is less than 190 EUR/ha. The highest average fixed rents are recorded in Zemgale, ranging between 370-375 EUR/ha. The highest agricultural land price this year was recorded in Rundāle Civil Parish of Bauska District, where the price per hectare approached EUR 14,865. In this case, a farm purchased a flat field spanning an area of 7.4 hectares.

In general, the number of transactions involving agricultural land decreased by 22% during the year. Up to the third quarter of this year, 1,715 transactions were registered, with 58 concluded in September. It is worth noting that the actual number of transactions may be slightly higher, considering the 1-3 month delay in data registration in the Land Registry. However, comparing the number of transactions in September of last year, there is a decrease of more than 70%. Last September, the majority of transactions occurred in Rēzekne District, as well as in Ludza, Krāslava, Valmiera, Bauska, Augšdaugava, and Madona Districts. This year, the demand for agricultural land remained in Krāslava, Augšdaugava, Cēsis, Dienvidkurzeme, and Talsi Districts.

The average price of forest properties in transactions involving the largest investors decreased by 11% in the third quarter of this year compared to the same period last year. The price per hectare is slightly more than 3,300 EUR, while clear-cut or forest land free of trees costs an average of 2,300 EUR/ha - a reduction of about 10% compared to last year. There is an observed drop in prices for mature coniferous (pine, spruce) forests. Last year, a hectare of forest, including the value of both the stand and the forest land, cost 26,000 EUR, while this year it costs 23,000 EUR. The price of medium-aged maturing conifer stands has decreased by 23%, equivalent to 13,000 EUR/ha, but the price of young conifer stands has remained stable at around 5,000 EUR/ha. On the other hand, the price of deciduous forest stands, with birch as the primary species, has remained unchanged: 17,000 EUR/ha for a mature stand, 10,000 EUR/ha for a middle-aged maturing stand, and 3,700 EUR/ha for a young stand. These two tree species are crucial in the market, holding a significant share in both the export and domestic markets.

The forest property market has experienced a slowdown in the past six months for various reasons, and it is crucial to recognize its close connection with the broader European context. Despite initial hopes for a stable sales and prices in Europe due to the previously introduced embargo on timber from third countries worldwide, current circumstances have not aligned with those optimistic forecasts. Considering the lingering effects of recession in Germany and Austria, coupled with inflation impacting the reduced consumption of manufactured goods, the demand for timber, lumber, and industrial products has seen a decline of approximately 15%. Timber prices, in particular, have reverted to pre-war levels, experiencing a one-fifth decrease compared to the beginning of the year. According to foreign experts, the prospects for improvement in the timber market are not anticipated until the autumn of the following year. This projection hinges on the expectation that more active construction and industrial activities will resume, consequently boosting the demand for Latvian timber in Western Europe. What was a profitable venture to buy brushland just a year ago is no longer the case. The costs of both wood chips and labor have risen. Latvia faces stiff competition, particularly from Poland, where labor costs are significantly lower, and Sweden, benefiting from a weakened krona, making it more economical to convert to the euro. This shift means that purchasing timber from Sweden has become notably more cost-effective.

“It is undeniable that the forest market is undergoing changes, yet it remains in motion. Forest owners are faced with the task of carefully considering the optimal course of action - whether to derive immediate satisfaction from the potential future value of the property after 100 years or to reap greater benefits by selling the property now and using the proceeds to fulfill current desires.

Observably, small forest investors, or private individuals, are steadily expanding their portfolios with modest forest properties. Their vision involves viewing these acquisitions as long-term investments for their pension funds or as assets to be passed on to future generations. In this way, these properties transform into family legacies, providing successive generations the opportunity to appreciate the wealth of Latvian forests and engage in their sustainable management,” says Jānis Vēbers, Head of the Forest Brokerage Department at "Latio".

* The agricultural land and forest property market is one of the most active real estate segments at present. Nevertheless, prospective transaction parties currently lack objective, publicly available information about the developments in this market segment. To promote the awareness of buyers and sellers, from now on "Latio" will publish the "Rural Property Market Index" quarterly, reflecting the current data of the market situation.

More information:

Jānis Vēbers

Latio | Head of Forest Brokerage Department

E-mail: janis.vebers@latio.lv

Mob. +371 29437967