Latviešu

Latviešu По-русски

По-русски In English

In English

In times of change, not only the residential sector of the real estate market is affected – changes also extend to commercial properties, pressuring owners to adapt to the current market situation. As several new Class A office buildings near completion, the hybrid work model introduced during the pandemic is driving demand for smaller and more energy-efficient office spaces. The market, responsive to global events, particularly the rise in interest rates and geopolitical uncertainty, experiences a decline in the share of large-scale transactions. This trend is evident in both the number of transactions and the composite index measuring investor confidence and interest. These observations are drawn from the latest Commercial Real Estate Market Report by agency “Latio”. Despite the reduced intensity, some substantial transactions are taking place, with property owners realizing that hoping for a miracle and expecting interest rates to drop soon are not justified.

The yields on commercial properties have remained unchanged over the last three and a half years. The highest yield (averaging 8%) is typical of industrial units. Retail spaces demonstrate a yield of 7.5%, while offices yield 6.7%. However, the highest activity is observed in the segment of new Class A offices. The New Hanza building in Skanste Neighbourhood has been put into service, the first building of the newly established business centre Gustavs has been completed, and the Novira Plaza and the business centre at 2A Pērses Street are also nearing completion. Additionally, the second round of the Press House Quarter [Preses nama kvartāls] development will be launched by the end of the year. The developer Linstow Baltic has received the green light for construction, with plans to launch the construction of the Satekles Business Centre soon. The concept of co-working offices is becoming increasingly relevant: the new Regus Business Garden complex has opened in Mārupe, Hamann Coworking has opened its doors in the renovated Hāmaņa Manor in Āgenskalns, and from next year, an innovative co-working workspace solution will be available on the 5th floor of the Galleria Riga shopping centre.

‘Latio’ estate agents have noted that owners of large office space (especially in buildings with lower energy efficiency) are facing difficulties in finding suitable tenants. Currently, small offices are in higher demand, serving the company's representative and social functions, hosting client appointments and management meetings, while the majority of employees work fully remotely or follow a hybrid work model. In a way, investors have already accepted the ongoing restructuring within the office market, recognizing that the demand for larger spaces is shrinking while demand for smaller ones is getting stronger. As a result, other office-defining factors are gaining focus. Prospective tenants are paying closer attention to nuances that were previously considered secondary, such as the amount of natural light and the energy efficiency class of the building. Here arises a conditional paradox; although it might seem that the available supply of lettable offices is extensive, and upcoming new office buildings will not achieve full occupancy, the demand for Class A offices remains high. This is because these offices adhere to the most up-to-date tenant standards, including flexibility in layout and adaptation to company needs. Class A offices are distinguished not only by prestigious locations but also by contemporary architecture, top-notch amenities, and the integration of technological solutions, thus validating the owners' set lease rates per square meter. The average monthly lease rates for Class A offices in central business districts in sought-after areas such as Skanste, Silent Centre, Near Centre, Ķīpsala, and Āgenskalns fluctuates between 13.5-22 EUR/m². For Class B offices, it ranges from 10-12 EUR/m², and for Class C offices, it ranges from 6-9 EUR/m². Outside the central business districts, the monthly lease rates for Class A offices is 12-14 EUR/m², for Class B offices, it's 9-11 EUR/m², and for Class C, it's 5-7 EUR/m².

During the first half-year, the industrial property sector in Riga and the surrounding areas experienced heightened activity. With an investment of 25 million euros, the construction of two industrial park buildings near the airport is set to commence soon. This includes the second building of the Green Park III warehouse complex, as well as the launch of construction for the second building in Airport Park III. Meanwhile, Baltic Electro Company intend to invest eight million euros in development of a substantial wholesale and logistics complex in Dreiliņi Neighbourhood. Furthermore, a modern PET recycling plant is being planned in Olaine, which is envisioned to rank among the European largest ones in the future. This ambitious project is being led by Eco Baltia company. While individual projects are progressing, there has been a broader shift in the interest of major investors towards impactful green energy initiatives across the Baltic region. These initiatives encompass various aspects, such as transformation of electricity transmission infrastructure, the development of wind and solar parks, and the formulation of innovative electricity grid solutions. It is anticipated that in the forthcoming years, investor focus will mainly concentrate on this specific direction.

"While similar patterns are evident throughout the entire commercial property market – a decreased transaction volume in the conditions of “tight money” – each subsegment reacts slightly differently to the current situation. It is obvious that purchase transactions in the industrial sector are occurring less frequently and at a slower pace. Overall, the need and demand from manufacturers for suitable production and warehouse spaces have not vanished, but we find ourselves in a pronounced imbalance period. It's clear that the “tight money”' significantly restricts entrepreneurs' ability to acquire new properties, especially among small and medium-sized businesses. The situation is even more aggravated by high construction costs and a limited supply of existing industrial units for sale, thus the prices are kept high. At the same time, it's important to note that industrial properties constitute only a portion of the entire commercial real estate sector," explains Artis Ramutis, the estate agent at "Latio."

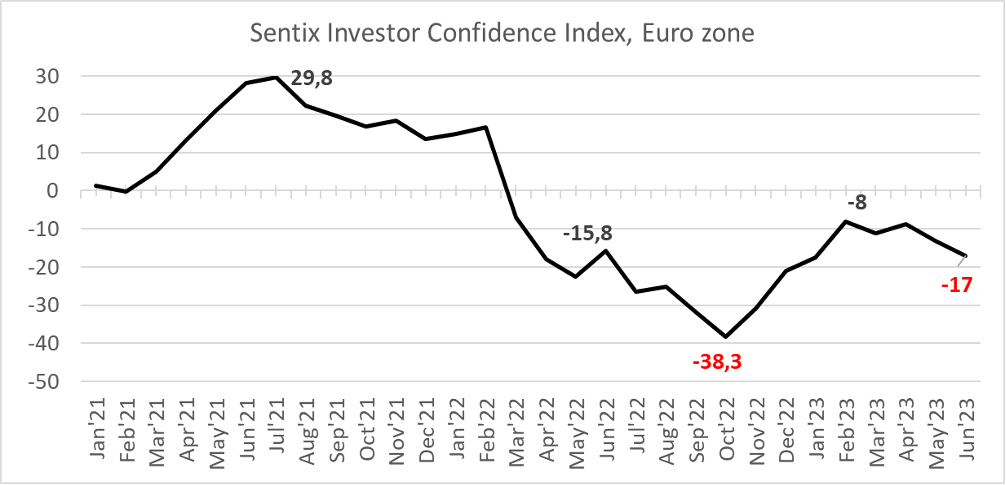

The sentiment of investors is clearly reflected in the international company "Sentix" investor confidence index, which analyses the economic outlook of the Eurozone over a 6-month period by aggregating data from nearly 3000 investors.

An index above zero indicates relative investor optimism, while below zero signifies scepticism in the market. The highest index reading in recent years was observed in June 2021, reaching 29.8 points. Since early 2022, the investor confidence index has not managed to recover from a significant decline. While the index was positive in February 2022, approaching 17 points, the geopolitical situation and related economic instability led to a plummet in October of last year, bringing the index down to -38.3. Despite some improvement in sentiment, with the index rising to -17 points in June 2023, pessimism among investors remains prevalent – as evident from the index curve that has continued to show a downward trend over the past six months.

Shopping centres have also improved their efficiency rates. While the growth momentum in the retail sector has slowed by more than 20% since 2019, a gradually rising trend was observed last year, evidenced by several substantial transactions. Initiating with an investment of nearly 22 million euros, the construction of a new Depo store began at Kārļa Ulmaņa Street, while the popular retail chain Lidl continues its expansion by opening new stores. In the first half of 2023, the monthly lease rates for retail space varied between 10-40 EUR/m² in the high shopping streets of the central district, and 6-10 EUR/m² for hypermarkets and the major (anchor) tenants.

In recent years, the rapid surge in transactions involving forest land has currently somewhat subsided. The average acquired area in certain regions has increased over the year: in Vidzeme, the average area in transactions is 10.6 hectares, in Kurzeme Region it's 9.7 hectares, and in Zemgale Region it's 9.1 hectares. However, when compared to the period from January to June of the previous year, the number of transactions involving forest land in the first half of this year has dropped by 46%. Until mid-summer, the prices for forest properties kept rising, yet they have now settled around just under 3000 EUR per hectare.

The decline in the number of transactions has also affected the segment of agricultural land commonly used for farming. In comparison to the first half of 2022, the total number of transactions has decreased by approximately 30%. The average sold agricultural land area in Vidzeme Region is 12.2 hectares, in Kurzeme Region it's 9.5 hectares, while in Latgale and Zemgale Regions it's just above 9 hectares. The highest average agricultural land price is in Kurzeme Region (4500 EUR/ha), and the lowest one is in Latgale Region (3450 EUR/ha). Meanwhile, the highest average rental rate in 2023 has remained consistently in Zemgale and Sēlija Regions, hovering around 235 EUR/ha.

“I would advise owners to be more courageous in the decision-making process, including anticipating price adjustments, and to respond to market conditions in a way that helps avoid unforeseeable risks in the future," believes A. Ramutis.